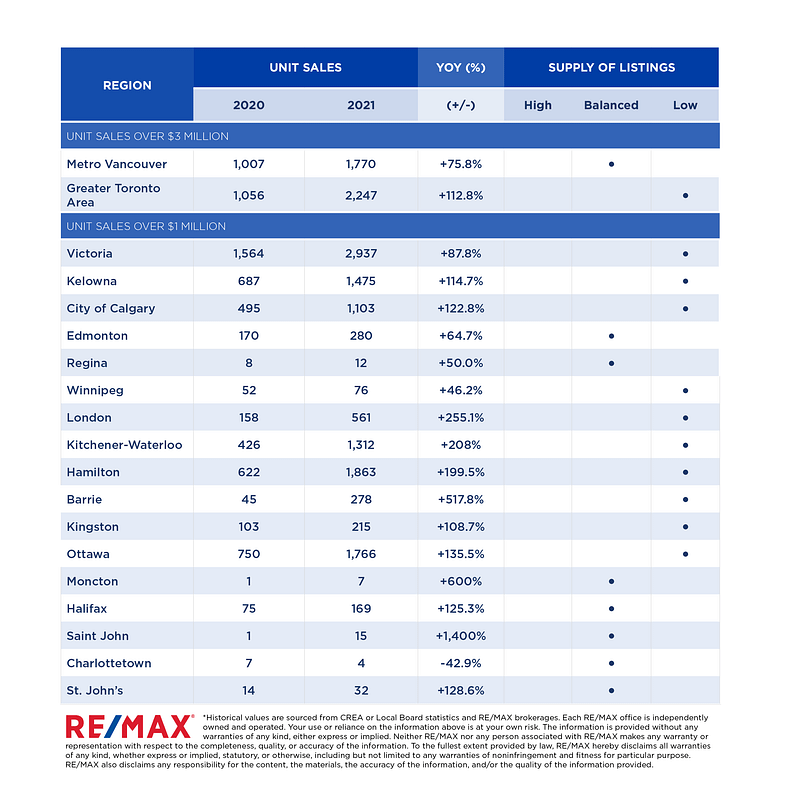

Okanagan centre has seen growth of 13.8 per cent from 2016 to 2021 to more than 144,500 people, latest census data shows

Kelowna, B.C. is officially the fastest growing city in Canada, according to the 2021 census data released February 9 by Statistics Canada.

Census figures show the Kelowna Census Metropolitan Area (CMA) has grown faster over the past five years that any of the other 40 CMAs in the country.

The Central Okanagan region, stretching from Peachland to Lake Country has a population of 222,167 — 14 per cent more than in 2016.

“I’m not surprised at all,” said Loyal Wooldridge, acting mayor of Kelowna and the chair of the Regional District of Central Okanagan.

“Seeing growth of 14 per cent sheds light on just how important it is that we have synergy in growth between our municipalities, because while certain council plan their municipalities or their First Nation, we have to be mindful that residents don’t see those borders.

“That’s why we are going through a regional housing strategy to understand the different OCPs [official community plans] spread across the partners and how that can create more synergies.”

Wooldridge says the unprecedented growth, not only across the region but within each of the six jurisdictions, makes it imperative that housing, transportation and environmental matters are balanced with an eye both regionally and municipally.

Statistically, Lake Country continues to be the fastest growing municipality in the Central Okanagan

Lake Country’s population, 15,817 is 22.4 per cent greater than the last census figures in 2016.

Kelowna, at 144,576, has grown by 13.5 per cent, West Kelowna (36,078) has grown 10.5 per cent while Peachland (5,789) has increased 6.7 per cent.

The City of Kelowna’s desire to move people from the outskirts of town into core areas seems to be working.

According to census figures, the city has the third fastest growing downtown of any CMA.

The downtown core grew by 23.8 per cent, behind only Halifax (26.1%) and Montreal (24.2%).

With a slowing of immigration due to the pandemic, much of the growth seen over the past two years specifically has been a result of migration from other parts of the province and country.

The Kelowna CMA benefited from the fact B.C. was the only western province which saw more people move in from other parts of the country than move out, a net gain of 97,424.

The City of Kelowna has forecast a population closing in on 200,000 by 2040, with 40,000 to 50,000 new residents expected over the next 20 years.